Introduction

Biodiversity, or NatureTech more broadly, has been receiving increasing attention from the media and VC investors in recent years, as recognition of our dependence on nature increases. Estimates suggest that 60% of global GDP is directly tied to biodiversity (UBS, 2024), which is eroding at a rapid pace, and this threatens to exert a sizeable impact on global business and our collective well-being. According to the NatureTechCollective, while there are $220Bn flowing into nature-based solutions every year (UNEP, 2026), nature still faces a $700Bn funding gap (NatureTechCollective, 2025). If this gap isn’t filled, McKinsey estimates that nature-dependent sectors like extractives, food and beverage, and apparel risk losing more than 40% of profits by 2030 due to nature risk, while others, like utilities, agriculture, and chemicals, stand to lose more than 10% (McKinsey, 2024). The first signs of this taking place are already apparent, with a recent wildfire liabilities claim leading to a major utility’s bankruptcy and a $5.4Bn settlement.

Furthermore, according to a report by Planet and Microsoft, over the past 50 years, wildlife populations have fallen an average of almost 70%, and this trend is bound to continue if no immediate action is taken (Planet, 2024). Given how interconnected and fragile ecosystems are, a rapid decline in one species can cause major and unexpected disruptions, introducing the risk of Black Swan nature events already in the coming decades.

As founders embark to build new solutions, they are bound to be supported by regulation, including the voluntary Taskforce on Nature-based Financial Disclosures (TNFD) framework, or the mandatory UK’S Biodiversity Net Gain (BNG) and EU’s Corporate Sustainability Reporting Directive (CSRD), among others. These regulations promise to mandate businesses to report and act on biodiversity, with strict penalties in place for those who fail to adhere. However, many long-time players in this field that we interviewed as part of this deep dive believe that regulation will likely be watered down or easy to game, and the first signs of this are already emerging. For example, according to one nature-tech founder, developers in the UK can easily circumvent BNG’s requirements by purchasing additional plots of land and simply planting trees on them, without investing in promoting biodiversity within the original development project, where it might prove more challenging. Moreover, these regulations introduce a number of challenges and trade-offs for policy-makers to process. Keeping with the same BNG example, one can see how smaller developers will have a harder time meeting the requirements imposed, and all developers will be put under additional duress.

The aim of this deep dive is to provide an overview of some of the greatest challenges we currently face in nature-tech, the solutions that are being built (with a focus on biodiversity/nature MRV tools), examine the role that regulation might come to play in advancing our collective efforts, and what we look for in meeting with founders crafting something in this space.

Market Overview

Based on recent data from Serena Capital and Crunchbase, funding in nature tech startups reached $2.1bn in 2024, growing 2x from 2019 levels.

However, $2.1bn is meager in comparison to the broader climate-tech VC, which hit a record last year of $40.5B with transport and energy being the main contributors (Sightline, 2025).

Investors we’ve talked to express a number of reservations that underlie the slow capital flow into the sector, including, but not limited to:

Low willingness to pay by end customers. Regulation for biodiversity and nature preservation is limited in most places around the world, and investing in biodiversity for businesses is often a luxury. While there are brands that support nature-based initiatives as part of their ESG policies or to market themselves as nature-friendly and charge a premium from their customers, such businesses are relatively few in number, and their investments are not substantial enough.

Difficulty in quantifying the nature impact. It is hard to measure the importance and impact of all things nature and biodiversity. What is the ROI of preserving a bird species on the verge of extinction? Is it higher than revitalizing the local flora? Such questions perplex nature proponents and inhibit many from effectively demonstrating measurable conservation outcomes (NatureTechCollective, 2025). This results in a gridlock and prevents further investment flows and effective regulation from being adopted. More generally, in economics jargon, it results in nature being treated as a common good and being unsustainably exploited.

Difficulty in monitoring the nature impact. Even if we could agree on a common methodology to value nature assets, monitoring remains an issue. According to one of the most extensive surveys of nature-tech organizations by the NatureTechCollective and Conservation International, which featured over 650 distinct enterprises, “critical gaps exist in biodiversity measurement capabilities.” (NatureTechCollective, 2025) This is especially apparent for project developers under BNG and other schemes, who are faced with the challenge of tracking species recovery and abundance (beyond just ecosystem health), while currently, there are no technologies for measuring these factors reliably. Moreover, according to Pivotal Earth’s (a biodiversity monitoring startup) 2024 report titled “Measuring nature and biodiversity: A guide to high-quality monitoring and analytics, “less than 7% of the earth’s surface has ever been measured methodically for the state of nature. A still lesser fraction is measured regularly enough to understand changes over time.” Monitoring, data collection, and analysis are key bottlenecks that prevent wide-scale understanding, pricing, and financing of nature-positive action. As a result, nature monitoring solutions and platforms built on top of them are an especially hot area for emerging startups and merit a special focus section found later in this deep-dive.

Problems in unlocking novel instruments to facilitate finance flows into nature. Sector mapping by the NatureTechCollective shows that 95 out of the 650 organizations are dedicated to experimenting with novel nature funding and monetization approaches (NatureTechCollective, 2025). These range from credit schemes to marketplaces to blockchain and NFT technologies. However, an extensive analysis of these organizations “reveals disconnects between data production and investment mechanisms,” (NatureTechCollective, 2025) which means that finance does not reach the optimal recipients in significant enough quantities.

Still limited use of AI and other latest advances. Only 80 of the 650 organizations surveyed in the NatureTechCollective report claim to leverage AI in their work (NatureTechCollective, 2025). From our conversations with founders and the aforementioned study, even within some of these organizations, adoption appears to be limited. On top of this, the EU’s 2024 AI Act and other emerging AI regulations threaten to classify some of AI's nature-based solutions, such as those affecting human livelihoods (think logging, wildfires, wildlife crime tracking, etc.), as “high-risk” algorithms, further impeding their development and dissemination. (Green Software Foundation, 2024)

Regulation is slow to be passed and threatens to make regulated businesses less competitive. In considering the measures to protect local ecosystems, regulators have to be careful in understanding that additional regulatory burdens will make it more difficult for businesses to operate and compete on an international level with counterparties that face no such constraints. For example, BNG, by forcing developers to report on biodiversity over a 30-year period after the project is built, as well as invest additional funds in enhancing the biodiversity of the site by at least 10%, might lead to fewer projects being undertaken and decreased housing supply, among other issues. Immediate socioeconomic needs of the populace are likely to win out over more abstract and long-term considerations pertaining to nature preservation.

Solutions Being Built

There are many different startups that have been operating or are only now emerging in the nature-tech space, ranging from earth observation aimed at tracking ecosystem health, to early wildfire detection and prevention systems, to nature-as-an-asset class valuation and fintech solutions. An expansive list can be found in this helpful nature-tech startup and non-profit list put together by Planet A and this NatureTechCollective report.

In digging through these startups, one is quick to find that many of them are regulatory bets that may or may not materialize in the next 5-10 years, while countless others are reliant on the notion of a green premium. In other words, they will hardly make for attractive business cases in the near future. That being said, there are also businesses that show tremendous promise. They differentiate themselves from the crowd in:

Tackling existing business needs with defined budgets. Instead of relying on green premiums or future regulation, these startups solve immediate and pressing business needs, often in the realm of resilience. For example, agricultural sector companies, manufacturing businesses with supply chains spanning many countries, and other such entities directly depend on the ecosystems surrounding them for smooth, continued business operations. Disruptions can cause millions in damages, and solutions that can help better understand and mitigate these risks can thus charge a high price. For instance, one startup we spoke to, Nios.earth, cited a case of a client in the textile/fashion space. This client was unaware that they were sourcing all their nylon from one supplier in a very high-risk area for droughts. Nios was able to identify the probability of a drought hitting the facility in the next few years and provide the client with guidance on how to diversify their supply chain to prevent disruptions.

That being said, extracting this higher price might not always prove easy. After spending time with companies selling nature-tech to these sectors, especially agriculture, we are slightly worried that these sectors might be too slow to adopt novel technologies or have trouble doing so with tight-margin-based budgets.

Going after high-probability high-impact events that affect specific communities and businesses. Think wildfire prevention around LA. Flood prevention and mitigation in historically high-risk areas. Since for these communities and businesses, nature-related risk isn’t highly theoretical and far off into the future, but immediate and potentially devastating. As such, it is also easier to quantify and price.

Taking a holistic approach to monitoring. No single data source can tell the whole truth about an ecosystem. And most regulations will require a complete view. Hence, it’s likely that individual monitoring solutions like satellite EO or eDNA will become inputs of high-value data platforms that tie everything up and provide analysis on top. But more on this below.

Experimenting with novel nature finance schemes. Apart from the aforementioned solutions in credits, marketplaces, blockchain, etc., we have also seen creative approaches like the one pioneered by Dots.eco or getsuperpower.com, which turn gamers into nature preservation funders by introducing exciting in-game challenges and items traded for real-life nature support vouchers. They also run promotional and loyalty programs for retail chains and other entities, and seem to be getting increasing traction.

Being highly scalable, ideally - AI-first. Many traditional nature-based solutions rely on outdated and messy spreadsheets, costly and time-consuming on-the-ground surveys by ecologists, etc. Like in many other areas, AI is bound to introduce significant productivity gains in nature-tech, and startups at the forefront of this are likely to emerge as winners in terms of scalability and cost-cutting. It is important to recognize that not everywhere is it feasible or desirable to completely remove ground-truth data collection by ecologists - for example, our conversations with industry experts and various studies confirm that remote sensing using satellites and AI processing remains vulnerable to cloud and forest cover, and “empty forest phenomena”, where satellite imagery indicates rich biodiversity but ground-truth data reveals facts to the contrary. (Aide, 2024) Apart from this, the only other real case for maintaining humans in the loop where it’s possible to remove them is the aforementioned AI regulation (Green Software Foundation, 2024), which could categorize AI-only systems as “high-risk” and thus slow down their adoption.

When it comes to AI, we would ideally like to see proprietary datasets, unique models, and other defensibility, as generic LLMs are progressing very rapidly and simple ChatGPT wrappers will prove easy targets.

Taking a regulation-agnostic stance or being frontrunners of it. This simply means that these businesses do not wait for guidance from various regulatory or advisory bodies. Often, the latter have little to offer - for example, TNFD recommends that businesses track the state of nature, but does not prescribe any metrics to use to measure it, leaving businesses scrambling to figure it all out for themselves. Innovative nature-tech startups, meanwhile, offer proactive ways to measure and assess, thus solving the conundrums businesses face, and potentially inspiring future regulation.

Focus: Nature Monitoring

There isn’t a general consensus on what is to be included or excluded from the nature-tech category. Here at Contrarian, we don’t invest in food-tech or ag-tech (for now, at least), so we chose to exclude them. Carbon is often included, given its interconnection with ecosystems, the many parallels between biodiversity and carbon credit schemes, etc., but at Contrarian, we treat ‘Carbon’ as a separate category, so it is also excluded. As a result, the biggest category in biodiversity/nature-tech that we’ve seen is, by far, nature/biodiversity MRV.

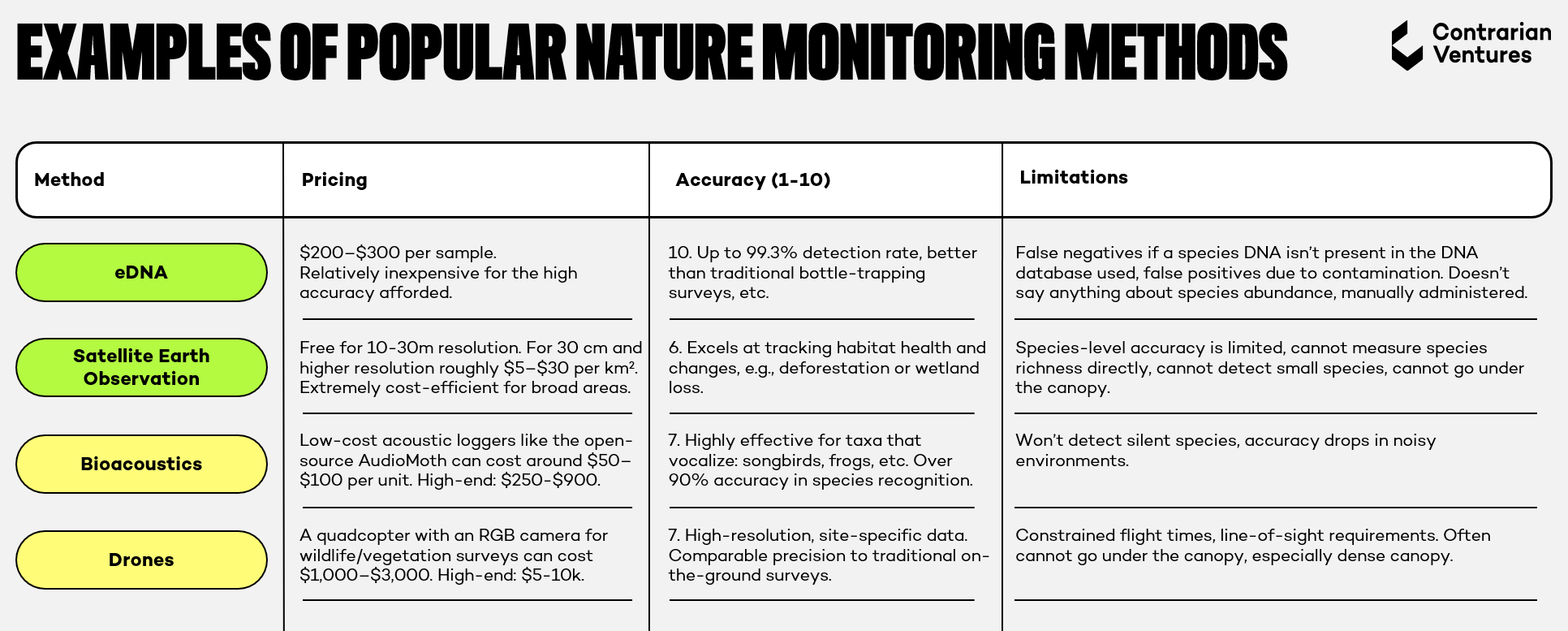

Nature and biodiversity monitoring, and the analysis required thereafter, are incredibly complex challenges. As mentioned before, they are all part of an intricate puzzle. Whether it’s satellites, drones, acoustics, eDNA, or other primary sources of nature data, they each constitute just a piece of that puzzle. Satellites help with imagery of large plots, but can’t go below the canopy. Drones offer a leg up in the resolution of these images, but also get stuck at the canopy level. Acoustics are helpful in that they cover a vast range of sound-producing species, but omit plant life and other measures surrounding habitat quality. eDNA can, in many instances, cover the broadest range of species, but says nothing about abundance and other important metrics. The table below provides a breakdown:

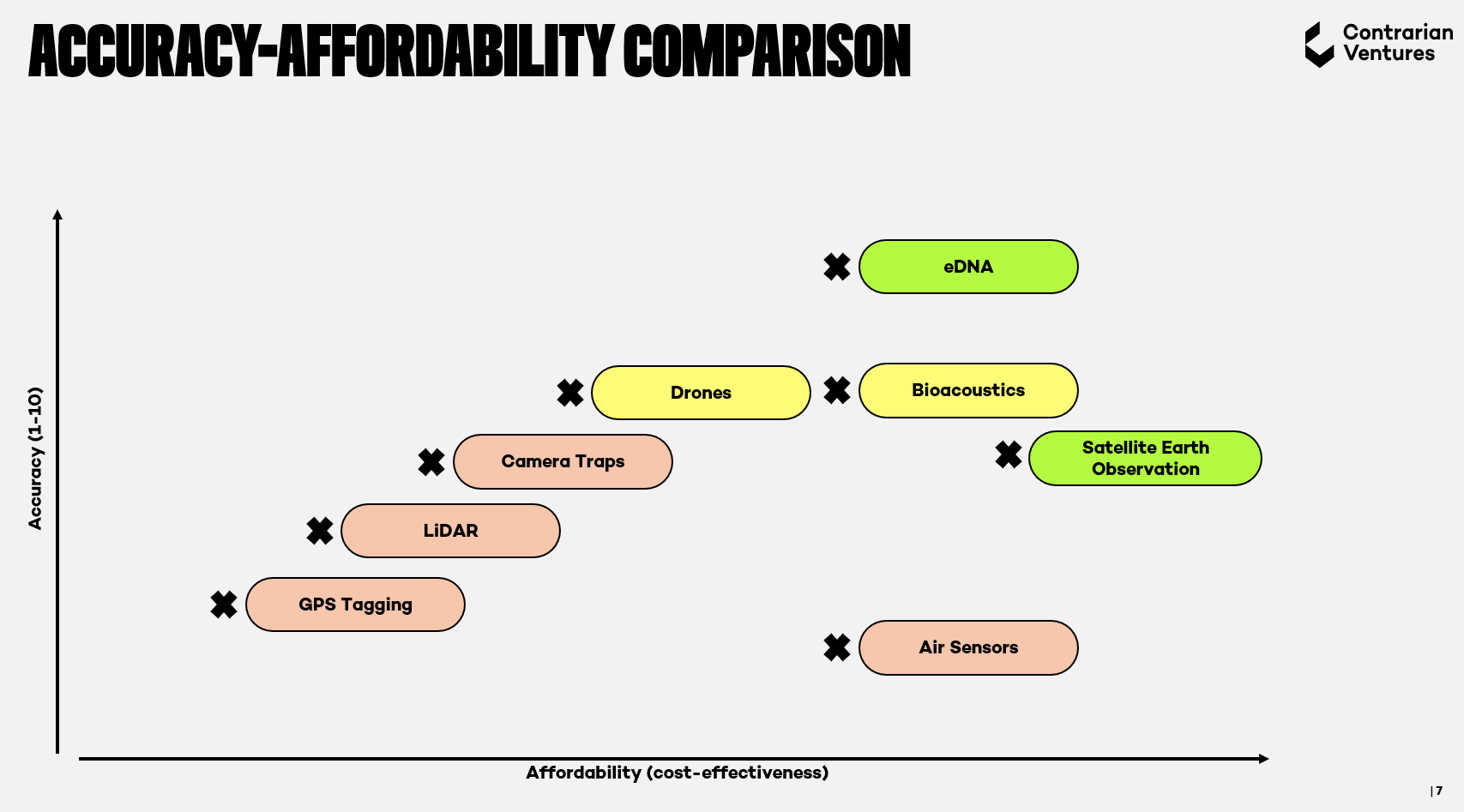

Then there are the slightly less popular and generally less efficient (of course, this depends on the context, use-case, etc.) methods like camera traps, LiDAR, GPS tagging, air sensors, community-based science apps and other ones, each with their own unique sets of advantages and disadvantages. As in the table above, it is helpful to compare these methods with one another in terms of accuracy and affordability.

It would be an interesting exercise to try and introduce an explicit third axis of scalability, which is now implicitly incorporated into both the accuracy (e.g., how wide of an area a solution can cover) and affordability (e.g., cost-effectiveness in terms of price per km²). However, this approach might bring more confusion than clarity, especially since a standardized comparison is inherently difficult here, given that each method is used in different settings and for different ends.

Given the limitations of each tool represented in the previous table, it is easy to see that all of them need to be used in tandem to provide for efficient primary data. Only with robust primary data can modelled data (extrapolations and estimates) prove accurate, but even then its accuracy reduces over time and individual site-level data inaccuracies can prove hard to pin down.

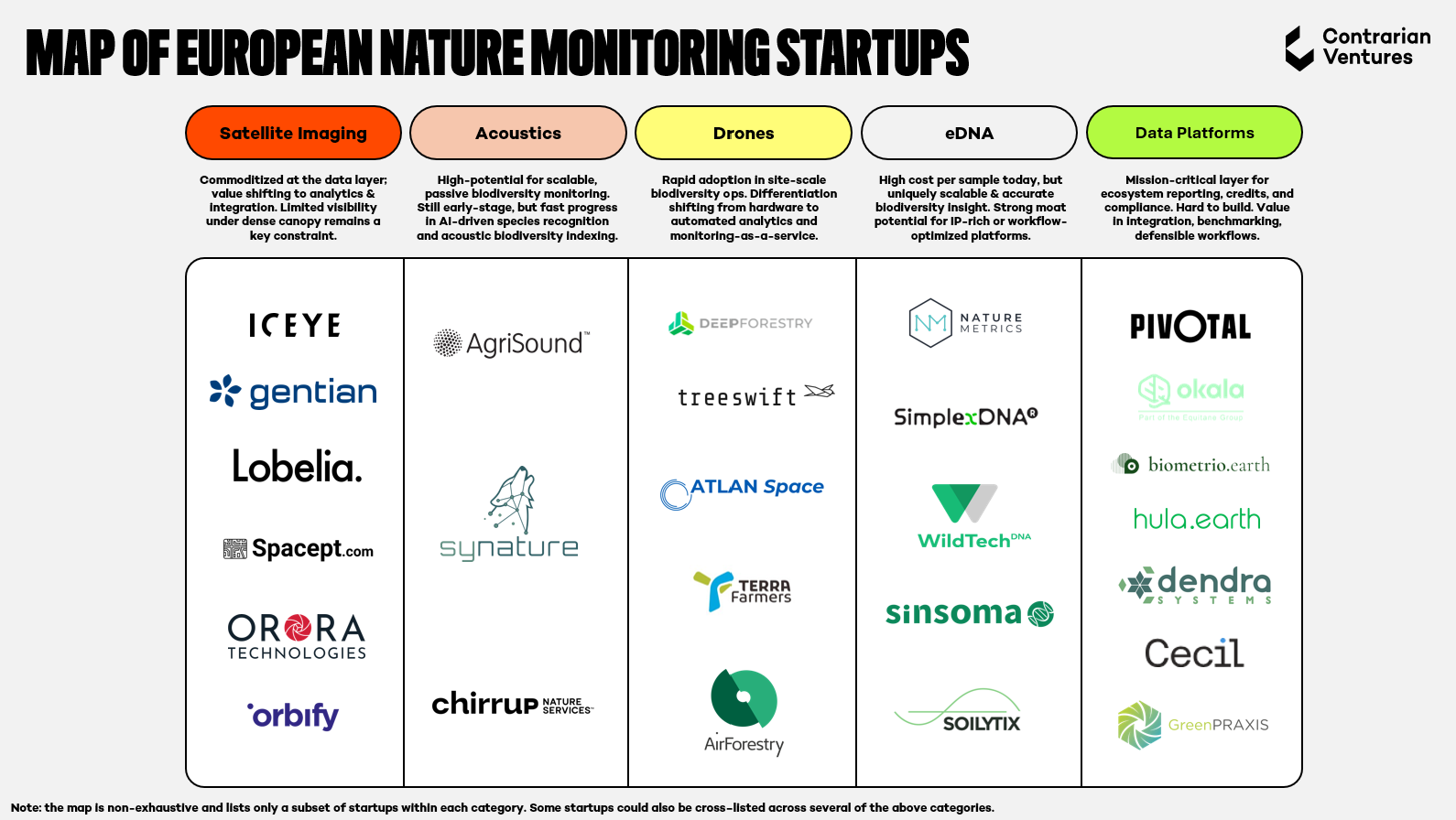

Data platforms that are able to bring all these individual monitoring tools together and provide a holistic view of an ecosystem offer the most exciting long-term business case, with most individual measurement tools becoming commoditized, in our opinion. Furthermore, the best platforms will be able to strike a good balance between the quantity, quality, and cost of data procured. A breakdown of the four most promising nature monitoring methods & data platforms, along with examples of such startups in the European ecosystem, can be found below. The map is non-exhaustive, and many other startups could be added under each category. The red-to-green scale indicates our excitement about each category with a brief rationale underneath.

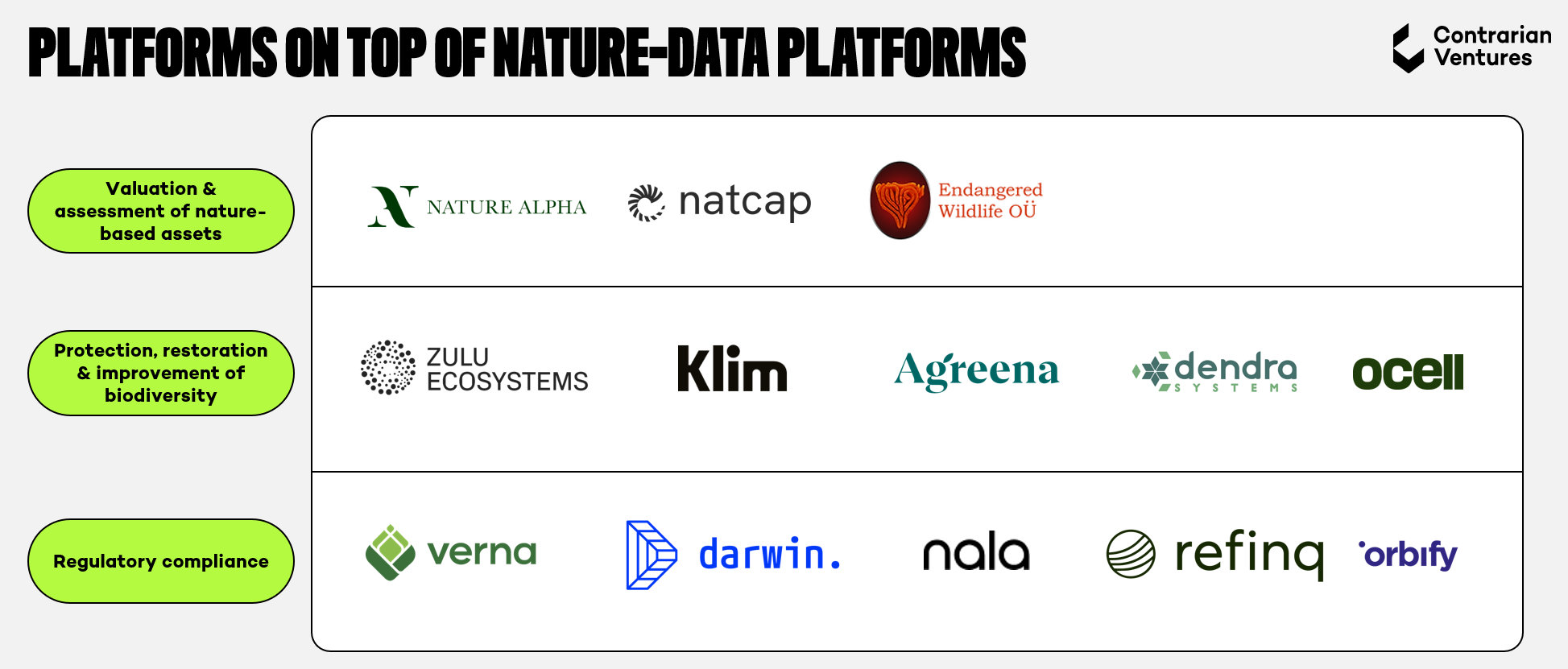

As primary empirical data is compiled and analyzed by nature data platforms, the next level of nature-platform businesses will be fully unlocked (made 100x more efficient, easy-to-use, and accurate). It includes, but is not limited to, the categories below:

It is too early to call the winners, but the foundational data platforms that integrate and accurately analyze primary data will likely be able to control the down-stream segment as well, including the above-mentioned categories of nature asset valuation, restoration and regulatory compliance. However, they might also serve as data providers to independent entities doing this work, which in itself is highly distinctive and complex.

Of these categories, the most challenging, as seen by the lack of startups attempting something like this, is properly valuing nature-based assets. If and when we develop accurate financial models and a “Bloomberg terminal for nature,” as one start-up we spoke to put it, the breakthrough will be in the same order of magnitude for nature and mankind as the invention of financial insurance. In other words, a real working solution here will be one of nature-tech’s greatest moonshots.

The Role of Regulation

Such moonshots as are needed to properly address the nature and biodiversity crises are rarely built by the private sector on its own. Collective action and state support are often needed. However, regulation around nature and biodiversity is still nascent, complex, and constantly evolving. There are a number of different frameworks for ecosystem reporting, ranging from the voluntary Taskforce on Nature-based Financial Disclosures (TNFD) to the mandatory EU Corporate Sustainability Reporting Directive (CSRD). These frameworks are often not aligned with each other and do not provide specific guidance on how each metric they outline should be tracked (Planet, 2024). This makes it difficult to ensure standardized and comparable reporting between companies and across time, not to mention among companies subject to different regulatory and reporting standards.

Among the different regulatory standards, the EU’s CSRD, with its European Sustainability Reporting standards (ESRS) E4 targeted at biodiversity and ecosystems, could be argued to be the most demanding and far-reaching nature/biodiversity reporting standard. It came into force in January 2023, with the first reports for 2024 due in 2025. The first batch of companies to report are large EU public-interest entities already subject to NFRD and meeting 2/3:

€50+ million in net turnover;

€25+ million in assets;

250+ employees.

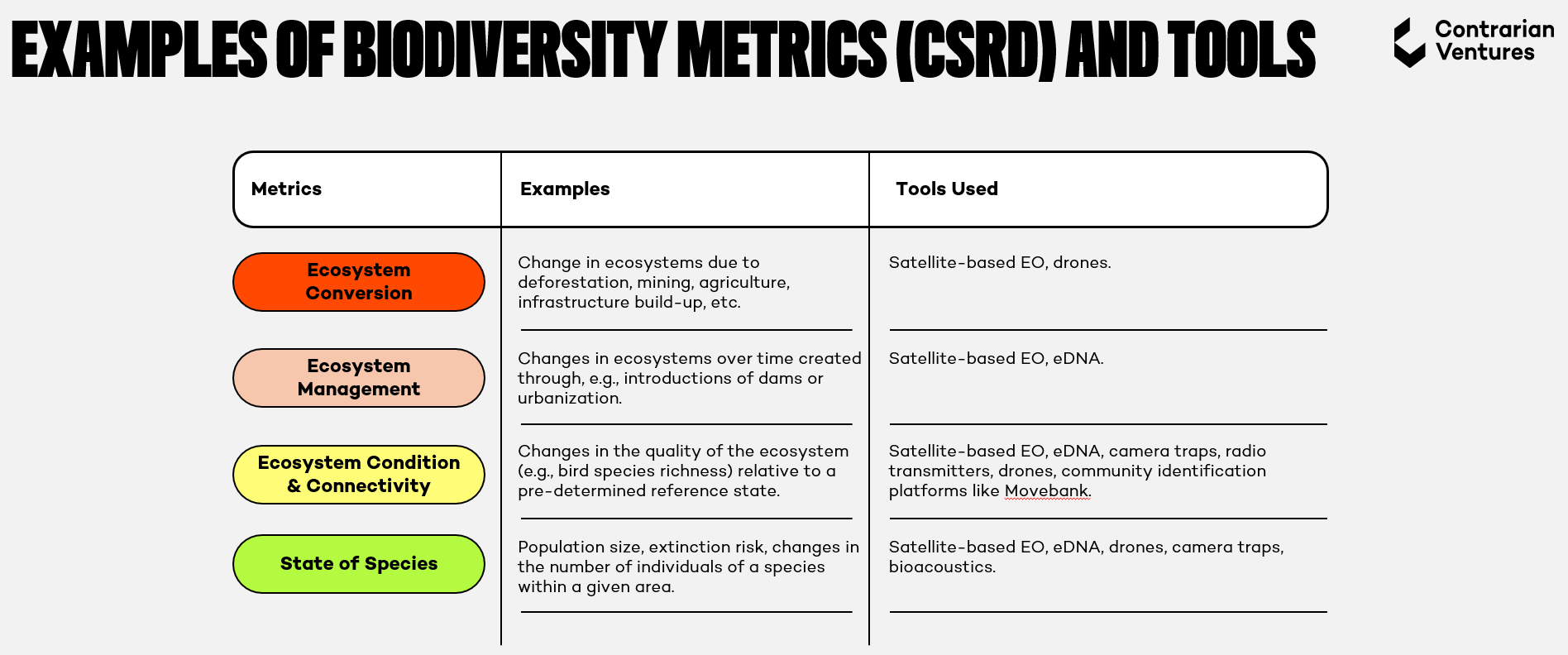

They are intended to be followed by large EU companies to report by 2026, SMEs by 2027, and non-EU companies with >€150 turnover in the EU by 2029. For those interested in the specific reporting requirements, reading the original legislation and the various supporting documents might prove helpful. Some examples of biodiversity metrics to be tracked under ESRS 4 can also be found in the table below:

All in all, CSRD, at least in its initial form, is a very ambitious piece of regulation and a step in the right direction in addressing the nature crisis. However, as mentioned previously, it is highly complex and threatens to overburden businesses with compliance requirements and red-tape, among the introduction of other undesirable side effects. Recognizing this, in February 2025, the EU announced the Omnibus Package, which significantly reduced the reporting requirements and introduced other important changes to CSRD. By December 2025, both a “Stop-the-Clock” directive and substantive amendments to CSRD had been formally adopted:

Increasing the employee headcount of companies subject to report from 250+ to 1,000+ — this effectively removes ~80% of companies from the scope of CSRD reporting, decreasing the total number of entities expected to report from 50,000 to 10,000;

Revising and simplifying the existing ESRS and rules, with EFRAG’s draft simplified standards published in December 2025 and a final Commission delegated act expected mid-2026;

A “stop the clock” policy that postpones reporting requirements for Wave 2 and Wave 3 companies by two years (to 2028 and 2029, respectively), while Wave 1 companies — large public-interest entities with 500+ employees — continue reporting as before.

Meanwhile, other policies across Europe, such as the EU Deforestation-free Product Regulation (EUDR), are also being delayed or significantly curbed (Global Witness, 2024).

This is all part of a larger trend, whereby, in a changed political climate, a new right-wing majority in the European Parliament is pushing back to undo the environmental and climate laws agreed upon following the 2019 election, known as the European Green Deal (Global Witness, 2024).

Across the English Channel, the UK’s BNG is facing its own set of similar challenges. After coming into force in February 2024, one year in, assessments indicated that less than half of the minimum amount of habitat expected has been delivered (Guardian, 2025). Moreover, recognizing the need to build housing and infrastructure, the UK government has proposed a bill that would significantly reduce the number of protected species surveys required for developments to be approved (Financial Times, 2025), among other measures, which threatens to cut 1,000s of jobs among ecologists and other environmental protection specialists. The UK government is also considering slashing BNG requirements for smaller and mid-sized developers, and housing projects up to 49 homes (SustainableViews, 2025). All this to say that BNG, too, is underdelivering and under threat of being significantly scaled back.

Overall, regulation serves as the first-mover where other incentives fall short, forcing companies to start thinking about nature and biodiversity or risk financial and other penalties down the line. For a while, it seemed like it might be a very important driver of progress in preserving the environment, especially within the EU and the UK. Many businesses were founded on this premise and are now in trouble, as policy-makers are introducing U-turns and reneging on their commitments. After extensive consultation with industry participants, we at Contrarian are pessimistic about the future of nature regulation in Europe and most countries across the globe and are thus looking to back startups that are regulation-agnostic and focused on existing commercial issues.

Conclusion

To sum up, present-day challenges to nature and biodiversity are immense. If not properly addressed, they threaten millions of lives and trillions of dollars in global economic output in the immediate future. However, since nature-assets are not effectively priced and tracking them is tremendously difficult, even with all the existing nature/biodiversity MRV solutions, nature is treated as a common good and unsustainably consumed.

While each business is contributing to solving a piece of the problem, strict regulation and outstanding technological advances are needed to solve it effectively. While signs of such regulation emerging were there a few years ago, most recently, policy-makers are coming to face the trade-offs between protecting the environment and meeting socioeconomic needs/supporting businesses, and are prioritizing the latter. More likely than not, whatever early legislation has been adopted or is being contemplated will be significantly watered down or reversed. This places even more pressure on innovative startups to come in and carry the burden of protecting the globe’s fragile ecosystems.

At the time of writing this piece, we see the biggest bottleneck within nature/biodiversity MRV. We need reliable data to understand what’s happening with nature. In particular, we need accurate monitoring tools and methods for different geographies, habitats, and other types of varying contexts, and platforms to bring these diverse sets of data together. We can then leverage this data to extrapolate and build models around nature pricing, risk, and other realms. With this data, we can also help companies comply with regulations and engage in nature restoration efforts. Here at Contrarian, we’re looking to back founders in the nature/biodiversity MRV space and nature-tech more broadly, especially founders who take a holistic approach, are AI-first, tackle existing business problems, promote resilience, and do not rely on regulation to succeed.

I thought climate/green/tech was over and now all the companies define themselves as resilient ones.